Kicking off a new year – and a new decade – is a great time to start thinking about resolutions, life goals and getting your financial house in order. Some of the basic steps to improving financial health are knowing where you’re at, where you want to go and establishing a clear plan on how to get there. Everyone has their own unique financial goals, whether that is saving to buy a dream vacation home, investing for a comfortable retirement or preserving family wealth. Here are some tips and starting points that will help you keep your financial plan on track.

Know your net worth:

Understanding your net worth is important, because it gives you a snapshot of your financial health and shows where you are at on the journey to realizing financial goals. Tracking your net worth over time allows you to evaluate your progress, as well as showing areas where you may need to adjust your financial plan to achieve specific goals or benchmarks.

Calculating net worth is a simple matter of listing assets at current estimated values and then subtracting any liabilities. Some common examples of assets are investment portfolios, cash, owned real estate, ownership in a business and other personal property such as art, jewelry, cars or boats. Liabilities are any debts that fall on the negative side of a ledger, which would include credit card bills, mortgage payments and other loan payments. It also is important to be realistic in assessing values to personal property, such as cars or boats, which can depreciate in value over time.

Create a financial plan:

Develop a financial plan that will help you achieve specific goals and objectives. Three components to a good financial plan are to understand how much you are saving; how much you are investing; and how much you are spending.

Certainly, spending money wisely is always prudent advice. However, the reality is that what one person considers “wise” or reasonable can be very different from another’s view. Start by creating a personal budget based on income and expenses for your own unique situation. You can’t manage what you don’t measure. Track income and expenses and create a budget that takes into consideration personal spending, as well as goals related to saving and investing. Does it have to be tracked down to the penny? Certainly not. But establishing general targets for saving, investing and spending is a more strategic, thoughtful approach rather than just hoping for the best.

Some good do’s and don’ts to use when creating a financial plan include:

- Do set specific goals, such as a target dollar amount to save for retirement or a major purchase.

- Do create a realistic budget that fits your personal lifestyle.

- Do prepare for emergencies that may include an unexpected home repair or health expense.

- Don’t forget to save for special occasions, such as weddings, anniversaries or graduations.

- Don’t forget to update budgets and financial plans as personal finances can and do change over time.

- Do ask for help. Not everyone is a do-it-yourselfer. Seeing assistance from a financial advisor can be beneficial in provide guidance, expertise and unbiased advice.

Know the difference between saving and investing:

People often say they are “saving” for retirement or “investing” for their future. In most cases, it is important to both save and invest as there are distinct differences between the two. Personal savings refers to money or property that has been put aside, oftentimes in a safe and secure place such as personal bank accounts, or government backed certificates of deposit or municipal bonds. In most cases, savings also are relatively liquid or easily accessible.

Investing generally means putting money to work so that the principal or original amount invested can earn income and/or appreciate in value. Some of the common types of investment products are stocks, mutual funds and real estate. However, investments span a wide variety of opportunities that range from acquiring an ownership stake in a business or copyright to a song to buying commodities, such as gold, timber or oil.

Another key difference between saving and investing is risk. Investing generally involves taking on some level of risk in order to achieve a return. One of the important steps to investing is understanding risk-adjusted returns. Low risk investments often result in low returns, while bigger risks have the potential to deliver higher returns. In either case, there are no absolute guarantees. So, it is important for individuals to understand the risks they are taking with their money so they can better decide whether the potential return is worthwhile. And it’s always a good idea to consult with a licensed financial advisor.

Wishing you a prosperous 2020!

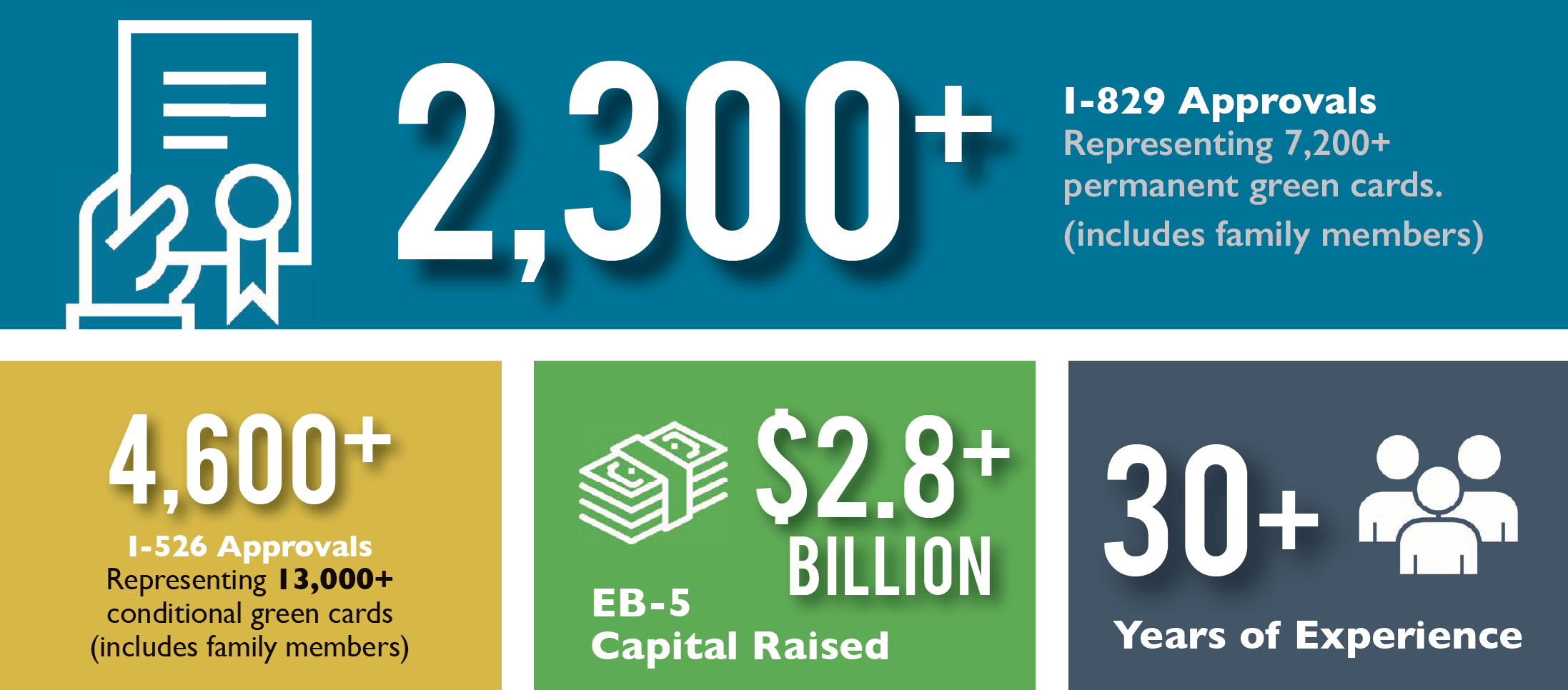

CanAm Enterprises, with over three decades of experience promoting immigration-linked investments in the US and Canada, has a demonstrated track record of success. With over 60 financed projects and $3 billion in raised EB-5 investments, CanAm has earned a reputation for credibility and trust. To date, CanAm has repaid more than $2.26 billion in EB-5 capital from over 4,530 families. CanAm manages several USCIS-designated regional centers that stretch across multiple states. For more information, please visit www.canamenterprises.com.